You may have seen headlines in the past week or so with big claims about a market downturn or a “bear market”. In moments such as this, it’s no surprise that you may have a few alarm bells ringing – if the markets are taking a dip, surely so is your investment portfolio?

The short answer is yes. But as you will know from our conversations together and the planning that we have worked closely with you to undertake, a temporary dip in the markets is nothing to worry about. Markets rise and fall all the time and evidence shows that in the long term, they always track upwards overall. We’re not worried, nor should you be.

What is a bear market?

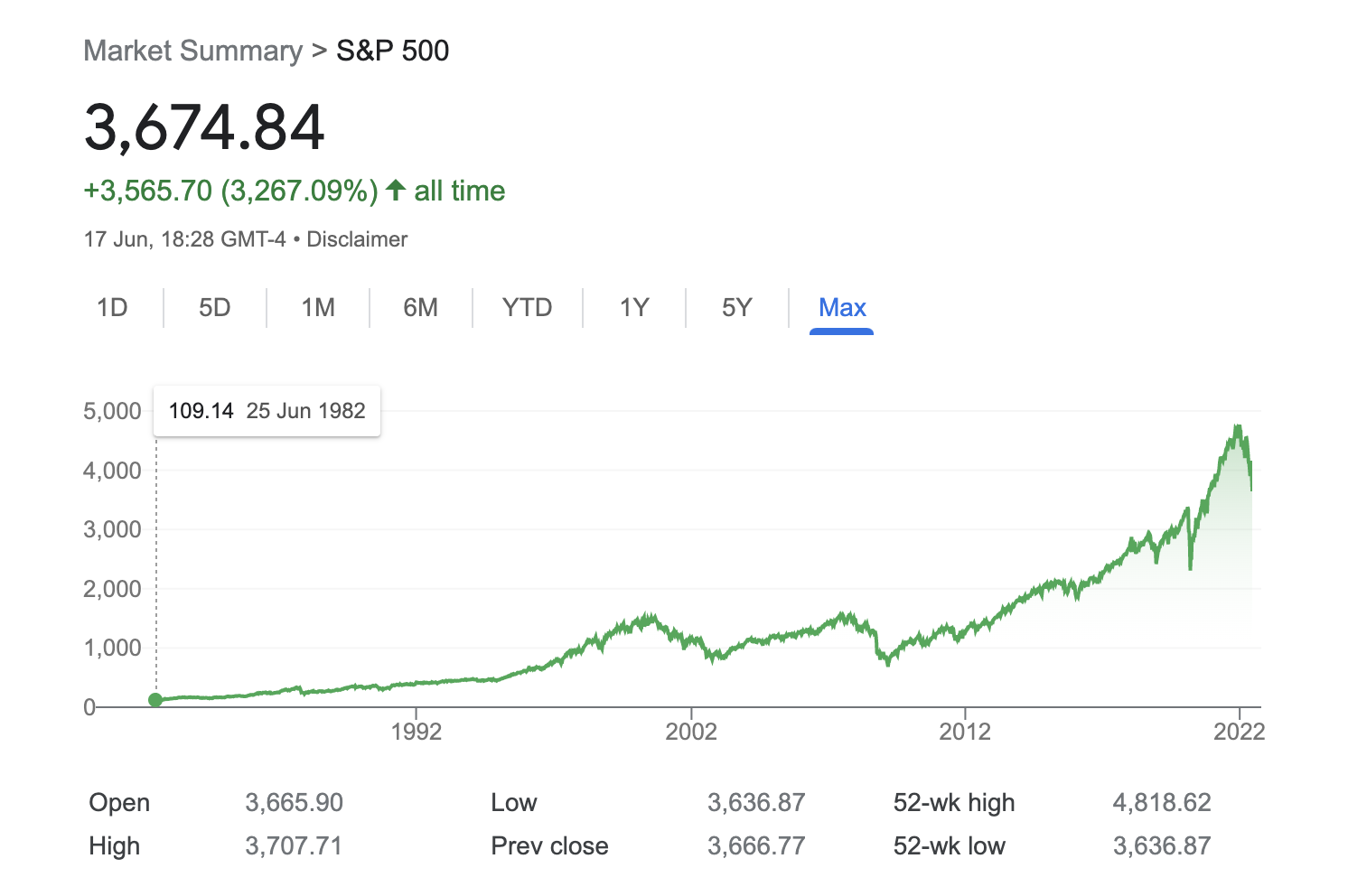

But you may be wondering what a “bear market” actually means. Typically, a bear market is the term for when a stock market’s prices fall 20% or more. The bear market that recent headlines are referring to is occurring in the S&P 500, which is a popular stock market index that tracks the performance of 500 large companies listed on exchanges in the United States.

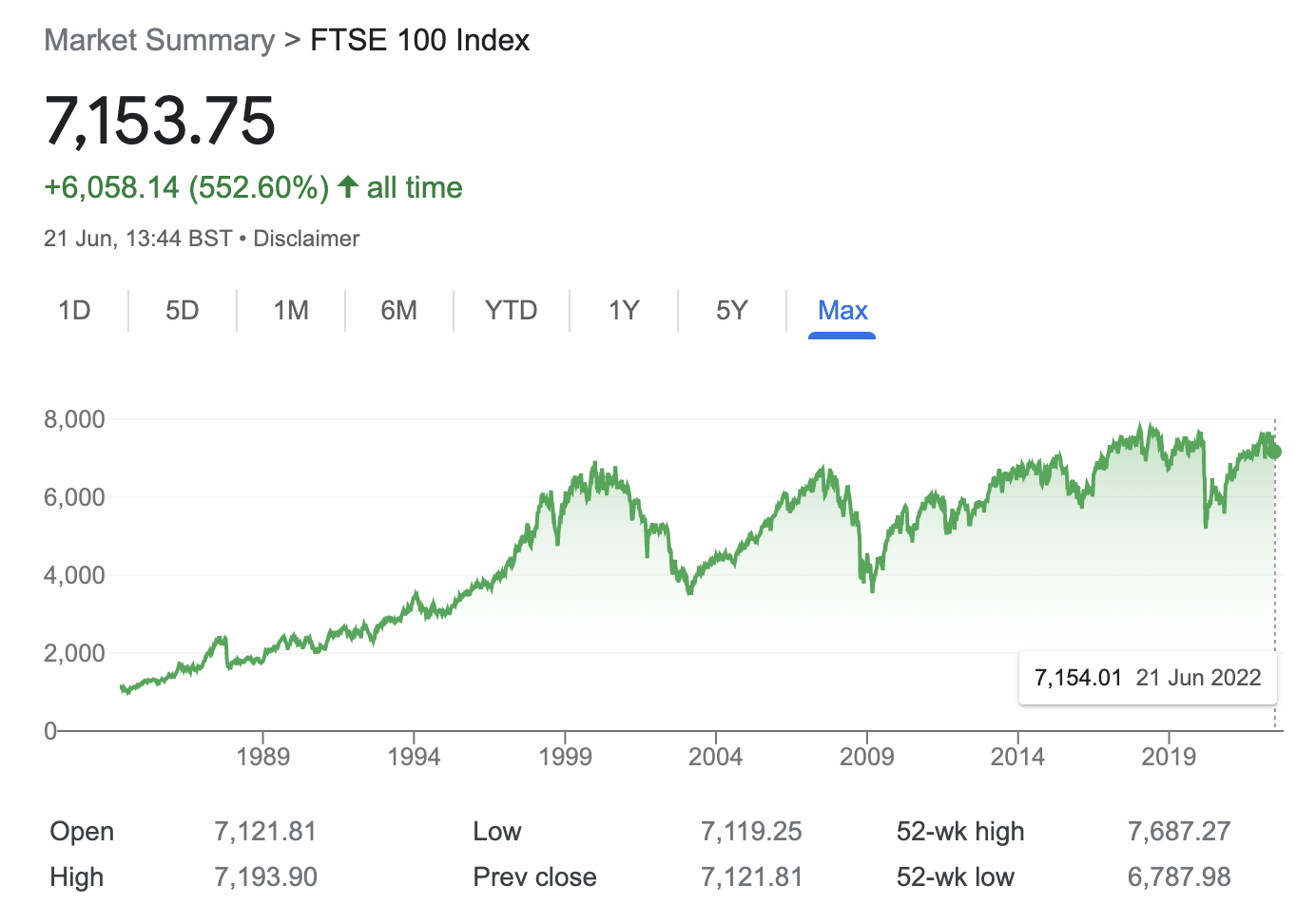

This chart shows the price of the S&P 500 index since 1982. While there are dips and bumps along the way, overall, the trend is for growth. The FTSE 100, the share index of the top 100 companies listed on the London Stock Exchange, displays the same upwards trend again over the long term – the graph below shows the index price’s growth since 1984.

This chart shows the price of the S&P 500 index since 1982. While there are dips and bumps along the way, overall, the trend is for growth. The FTSE 100, the share index of the top 100 companies listed on the London Stock Exchange, displays the same upwards trend again over the long term – the graph below shows the index price’s growth since 1984.

There is always new wealth being created in the world, so unless something truly catastrophic happens and society as we know it falls apart, new wealth will continue to be created and the markets will continue to increase in value.

When we work with your financial plan, and in particular your investment portfolio, we’re not looking at the short term. We’re focusing on the long-term – more than 10 years into the future – and both our own experience and the reams of evidence available to us mean that we are confident in a bountiful future and a life well lived for you and your family.

What should I do now during this market downturn?

Nothing at all. Of course, if you are worried and would like to talk it over with a member of the team, please don’t hesitate to give us a call. But your portfolio is carefully designed and balanced to weather and withstand rumbles in the market and is diversified enough to ride the storm.

In the past, after big declines, the stock market has always come back. Over 10-year periods, if you had put money into the entire S&P 500 you would have lost money only 6 percent of the time. Over 20-year periods, you would never have lost money. It’s a similar picture for the FTSE.

What about the interest rate increase?

This is one area where you are likely to feel the effects more or less straight away. We’ve all heard plenty of discussion about the rising cost of living and more than likely experienced it. In fact, if you’ve put fuel in your vehicle at any point in the past few months, you definitely have.

The Bank of England’s interest rate has risen again to 1.25% from 1%, making it the fifth consecutive rise. Inflation is currently at a 40-year high of 9.1% at the time of writing. However, your personal inflation rate will depend on what you spend your money on – and how much goes on each element.

In real terms, this could mean:

- An increase in your household food bill

- Higher fuel and energy bills

- Higher rates on any mortgage repayments you may be liable for

- Your interest rate on your savings accounts may go up (but not at a rate high enough to counteract inflation)

Will my cost of living go up?

Possibly. As the official rate of inflation is based on the average price of a common basket of goods and services, the extent it will actually affect you will depend on what you buy. While energy prices soared 23.2%, for example, clothing averaged 6.3% and food was at 4%. So, consider whether you can adjust your spending habits to lessen some of the bigger shocks without compromising your quality of life too much.

If you are unable to tweak your expenses enough to redress the imbalance with what is coming in, you may find yourself in need of access to more income than you are currently drawing. If this is the case, please get in touch with us at your earliest convenience and we’ll be happy to assist you.

In summary, the next few years are likely to feel a little squeezed in terms of spending power and cost of living. But with your financial plan securely in place and your investment portfolio doing what it’s designed to do in the background, any uncertainty in the market should be cushioned and your plans for your life should still remain intact.

__

If you would like to discuss any of the topics we have covered in this article, you can contact us by telephone on 02920 782330 or by email at theteam@uniqfamilywealth.co.uk.

Please note we operate a four-day working week and therefore our lines are not manned on a Friday or on weekends.